Money matters

Debt Investment options for your retirement corpus

The next step in our asset allocation series looks at debt investment options

Retirement can be a golden phase if you plan right. During these years, most people would like to lead a healthy, tension-free life and have a good night’s sleep without being bothered about finances. Debt instruments are perfect in that sense. It brings stability and ensures capital preservation. At least 40-50 per cent of the retirement portfolio can be parked in debt instruments at the age of 60 years. The ratio can be increased further as age increases.

Investment Options available

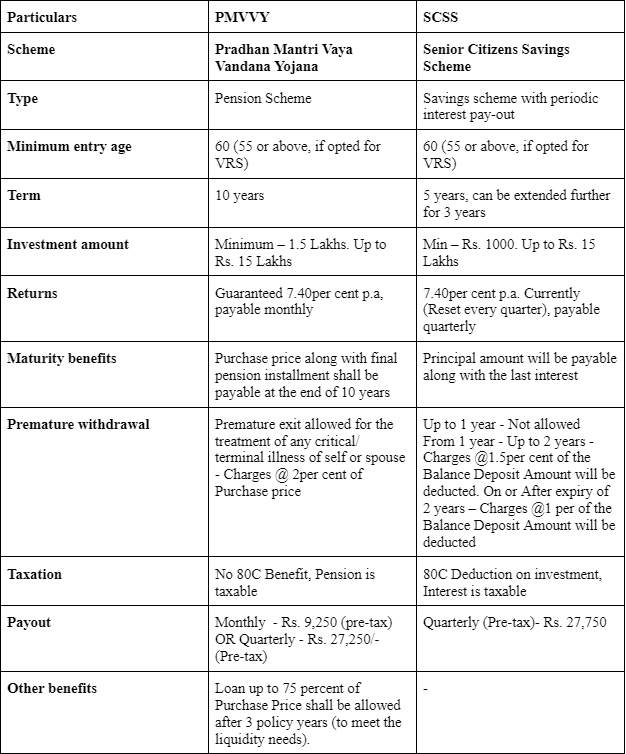

A) Government Schemes

- Senior Citizens Savings Scheme

- Pradhan Mantri Vaya Vandana Yojana

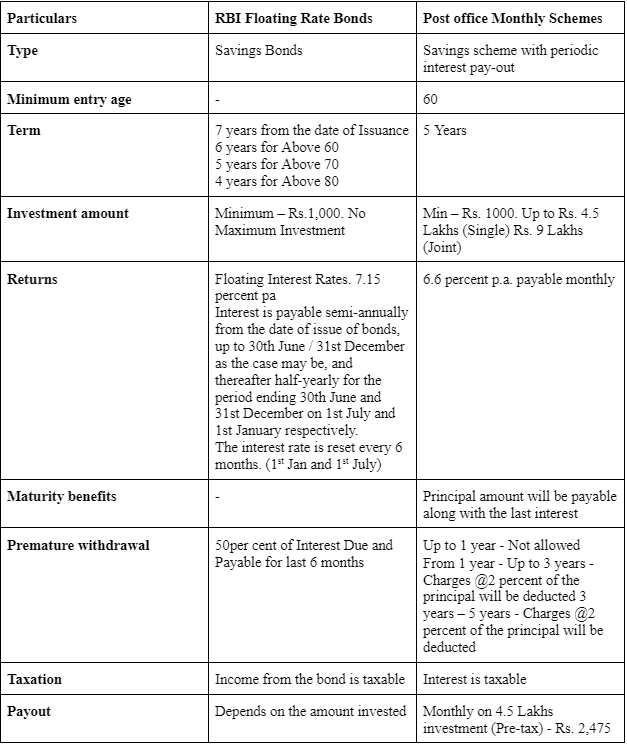

- RBI Floating Bonds

- Post office Monthly Savings Scheme

B) Other Investment Options

- Fixed Deposits

- Mutual funds

Fixed Deposits:

Fixed deposits offer a return of around 4 per cent and 6 per cent (pre-tax) on 5-year deposits today. Fixed deposits have lock-in and hence it carries reinvestment risk. This will not help us to beat inflation in the long run. In the case of fixed deposit, 10 per cent TDS is deducted on interest every year irrespective of deposit maturing.

Debt mutual funds & SWP:

You can ensure regular cash flow by withdrawing from a growth liquid fund every month. Reinvestment risk in FD can be overcome with SWP in debt funds. The gains are taxed at the time of redemption. Depending on the duration held, capital gain tax can be short term or long term No TDS is deducted on debt funds. The tax is payable on redemption which makes compounding gains more efficient.

Disclaimer: Consulting a professional can always help you to identify the right avenues for investments during the golden years.

For Part 1 of this series see here: How To Allocate Your Retirement Corpus

Photographs courtesy: Pixabay

Comments

Post a comment